Blockchain is becoming mainstream. For many in the crypto community, this acceptance is long overdue. However, as with any new emerging technology or industry (e.g. artificial intelligence or marijuana legalization) there remains a fair share of skeptics; those who are comfortable with the status quo and are quick to point out flaws in the system, opportunities for misuse, and the potential for the already disenfranchised to be further taken advantage of. For those of you who are cautiously optimistic and want to learn more about blockchain, we want to debunk some of the popular myths for you.

Skeptic or not, blockchain technology will likely make its way into your life and sooner than you think whether it’s being able to track the journey of your food to your plate, easily send money to family or friends across borders, track the provenance of luxury items or prescription drugs, speed up the escrow process, safeguard elections, etc.

The advantages of blockchain technology must be weighed against the technology’s limitations when deciding whether it’s the right approach for you. Knowledge is the first step; hopefully by the time you get to the last paragraph, you’ll have a better understanding of blockchain technology, how it’s currently being used and even some of the challenges to adoption.

Myth: Blockchain = Bitcoin

Many people’s first exposure to the term “blockchain” is when they’re reading about Bitcoin; many think blockchain is Bitcoin and use the terms interchangeably. This is probably the most common misconception about blockchain. Blockchain first entered awareness with the introduction of the digital currency known as Bitcoin in 2008. A few years later, people realized that blockchain, the underlying technology powering Bitcoin, had other uses beyond digital currency.

A blockchain is essentially an open, decentralized ledger that records transactions between two parties permanently without requiring third-party authentication. Next came Ethereum, a smart contract platform created to address what its cofounders saw as programming limitations of Bitcoin’s blockchain. Smart contracts are computer programs that execute when predetermined conditions are met. Today, there are countless blockchains and smart contract platforms.

Here’s an analogy that may help: in the early 90’s email brought the internet to the general public and the same type of confusion ensued; email is the internet, right? Of course by now, we all understand that is a ridiculous statement. The internet is simply the engine that powers email. Can you send an email without the internet? No. Can Bitcoin exist without blockchain? No. Just like the internet, blockchain technology will power, automate and improve many aspects of our lives.

Working on a smart contract or blockchain-based application? Interested in Esprezzo's smart contract templates, API, SDKs or bridge technology? Reach out to learn more about our pilot program.

Myth: Blockchain can only be used to power cryptocurrencies like Bitcoin

Not to be repetitive, but this is also false. Similar to the idea that blockchain is Bitcoin, many people believe that blockchain technology’s only use case is to power cryptocurrencies when in fact, many business processes and industries can benefit from the underlying technology that is blockchain. From healthcare, to finance, real estate and insurance, the applications for blockchain technology are vast and we’ll get into this more later. Cryptocurrencies are simply the first phase in the long arc of blockchain adoption.

Soon you’ll see publications proclaiming the revolutionary efficiency of smart contracts powered by the Ethereum protocol which has a developer network twice the size of Bitcoin. From MLB Crypto Baseball Cards to Cryptokitties and other digital collectibles to purchasing real estate, the number of applications for blockchain and the networks they run on are only likely to increase in the future.

The potential and broad applicability of blockchain technology prompted The Linux Foundation to create Hyperledger, an ‘umbrella for open source blockchain & smart contract technologies’. As explained on Hyperledger’s website:

“Not since the Web itself has a technology promised broader and more fundamental revolution than blockchain technology. A blockchain is a peer-to-peer distributed ledger forged by consensus, combined with a system for ‘smart contracts’ and other assistive technologies. Together these can be used to build a new generation of transactional applications that establishes trust, accountability and transparency at their core, while streamlining business processes and legal constraints.”

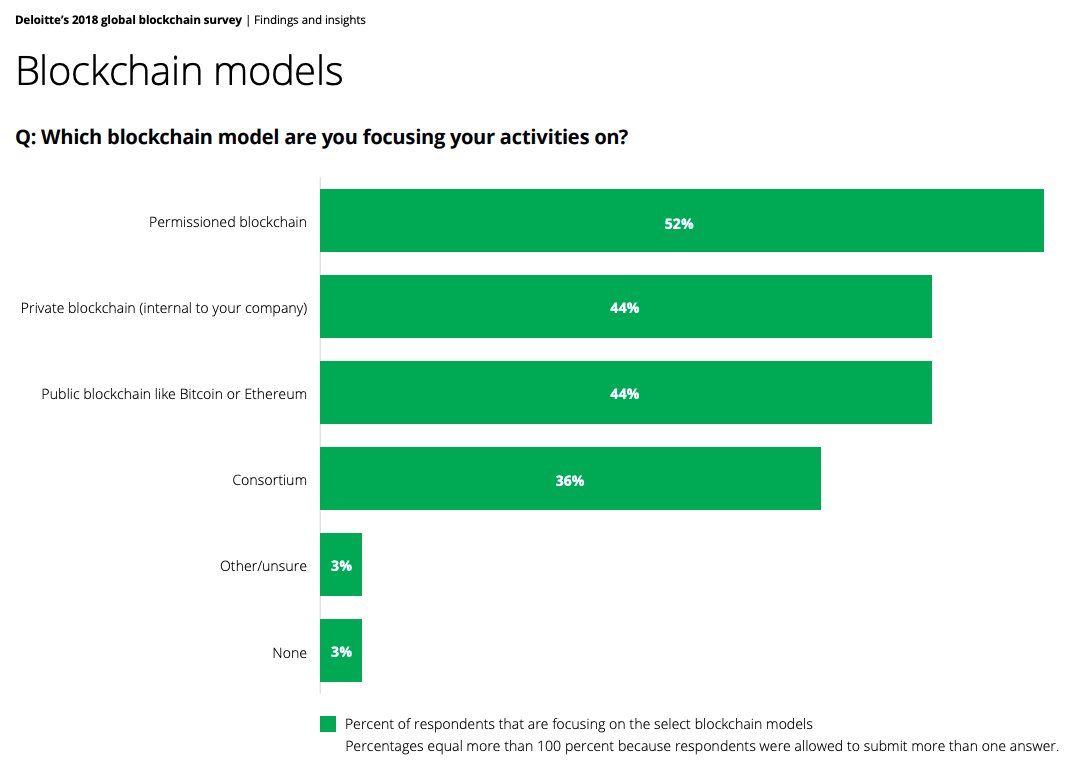

Myth: All Blockchains, and All Information on Them are Public

This is false. While Bitcoin, Ethereum and many of the most well-known blockchains, are public, meaning the network is completely open and anyone can participate in the network, private (permissioned) blockchain networks exist and may be a preferred solution for certain use cases. Many vibrant private and semi-private blockchains exist; Hyperledger and Corda are all examples of this. While on a public blockchain, all transactions are completely transparent and anyone can participate in the consensus process whereas “permissioned” networks are exactly what they sound like, you need “permission” to participate. Here’s a more in-depth breakdown of public versus private blockchains.

Source: Deloitte's 2018 global blockchain survey

Private and semi-private blockchain networks are more likely to be utilized by businesses that have select, known parties they conduct business with, sharing immutable information information with one another, in real-time (think all members of a manufacturing supply chain, or stakeholders conducting international transactions). Also, permissioned networks typically use a proof of stake or proof of authority consensus mechanism rather than proof of work (like Bitcoin). Evaluating the pros and cons of consensus mechanisms is a must when evaluating which blockchains meet your needs and match your philosophies.

Myth: Blockchain is the best solution for everything

When you hear a blockchain evangelist speak, you’d think this revolutionary new technology is the panacea for all earth’s qualms. And while we wish this were true, it isn’t. Blockchain technology is great at certain things and not so much when it comes to others. With benefits including increased transparency, immutability and efficiency, it’s easy to understand why many are so enthusiastic about blockchain’s potential. However, blockchain is not a silver bullet, and the decision to implement blockchain into your tech stack requires planning and consideration. There are times when traditional databases may make more sense.

Here’s a handy compilation of flowcharts with different models to answer the “do I need a blockchain” question. Factors to consider when deciding whether blockchain makes sense for your business or project include whether all participating parties are known or trusted, complexity of business logic, the need for a shared, consistent data store, how many entities need to contribute data and whether public verifiability is required. If you decide that blockchain makes sense for you, you’ll also want to think about what data makes sense to store on-chain vs offchain; moving computation and data off-chain can help offset concerns about performance and scalability.

Supply chain tracking, legal, and cross-border financial transactions are a few examples that benefit from the use of blockchain technology; multiple parties are involved, and traditional business operations required people locating records, verifying that all agreed-upon transactions have been met — processes that used to take days and weeks can now take hours, minutes or seconds.

Myth: Blockchain technology isn’t ready for business adoption

Many people believe that concerns surrounding privacy, security and performance make blockchain inadequate for business adoption. A lot of that may be due to the misconception that blockchains are all public and open, as mentioned above. Some hesitance is also to be expected as is always the case with new technologies that are first explored by pioneers and visionaries and only take hold of the masses once repeatable, referenceable examples of ROI are published.

Source: Deloitte's 2018 global blockchain survey

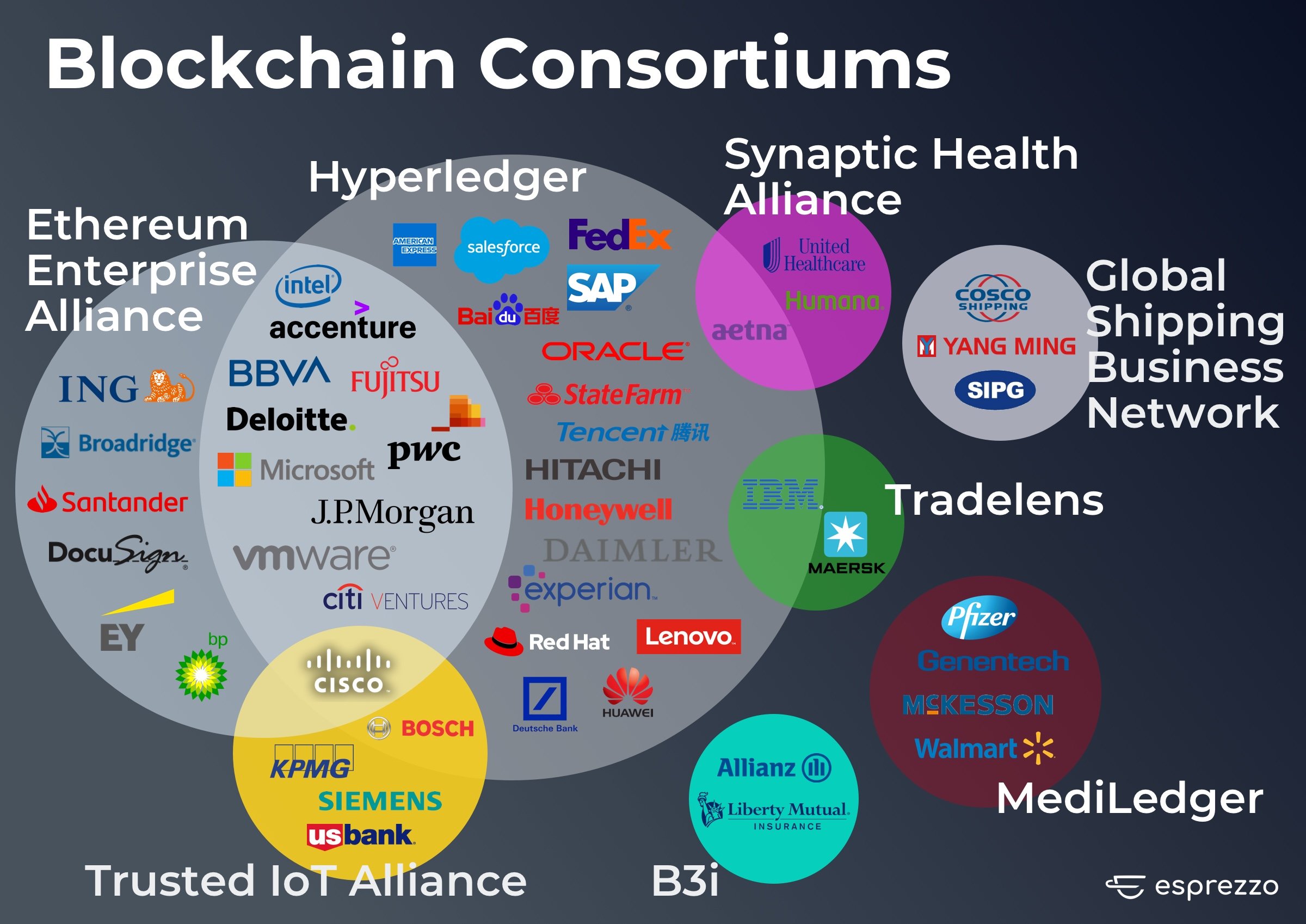

In the last few years, industry and platform-specific blockchain consortia have sprung up and play a key role in educating businesses as well as driving innovation and standards. Here are a few of the popular ones, with a non-inclusive list of members:

- Enterprise Ethereum Alliance — Accenture, BBVA, Banco Santander SA, Cisco, Deloitte, DocuSign, Ernst & Young, ING Bank, Intel, JP Morgan, Microsoft, PricewaterhouseCoopers, VMware

- Hyperledger — Accenture, American Express, Baidu, Cisco, Deutsche Bank, Daimler, Fujitsu, Hitachi, IBM, Intel, JP Morgan, SAP, Aetna, BBVA, Bosch, Citi, Deloitte, Experian, FedEx, Honeywell, Huawei, Lenovo, Microsoft, Oracle, PricewaterhouseCoopers, RedHat, Salesforce, State Farm, Tencent, VMware

- B3i (insurance) — Allianz, Liberty Mutual

- MediLedger (pharmaceuticals) — Pfizer, Walmart, McKesson, Genentech

- Trusted IoT Alliance (Internet of Things) — Bosch, Cisco, KPMG, Siemens, US Bank

- Synaptic Health Alliance (Healthcare) — Aetna, Humana, United Healthcare

- Global Shipping Business Network (supply chain) — COSCO Shipping Lines, Yang Ming, Shanghai International Port Group

- TradeLens (supply chain) — IBM, Maersk

As you can see, many companies have come together to explore solutions for challenges around privacy, security and performance, and are continuously working towards setting industry standards that will lay the foundation for mainstream business adoption.

Source: Deloitte's 2018 global blockchain survey

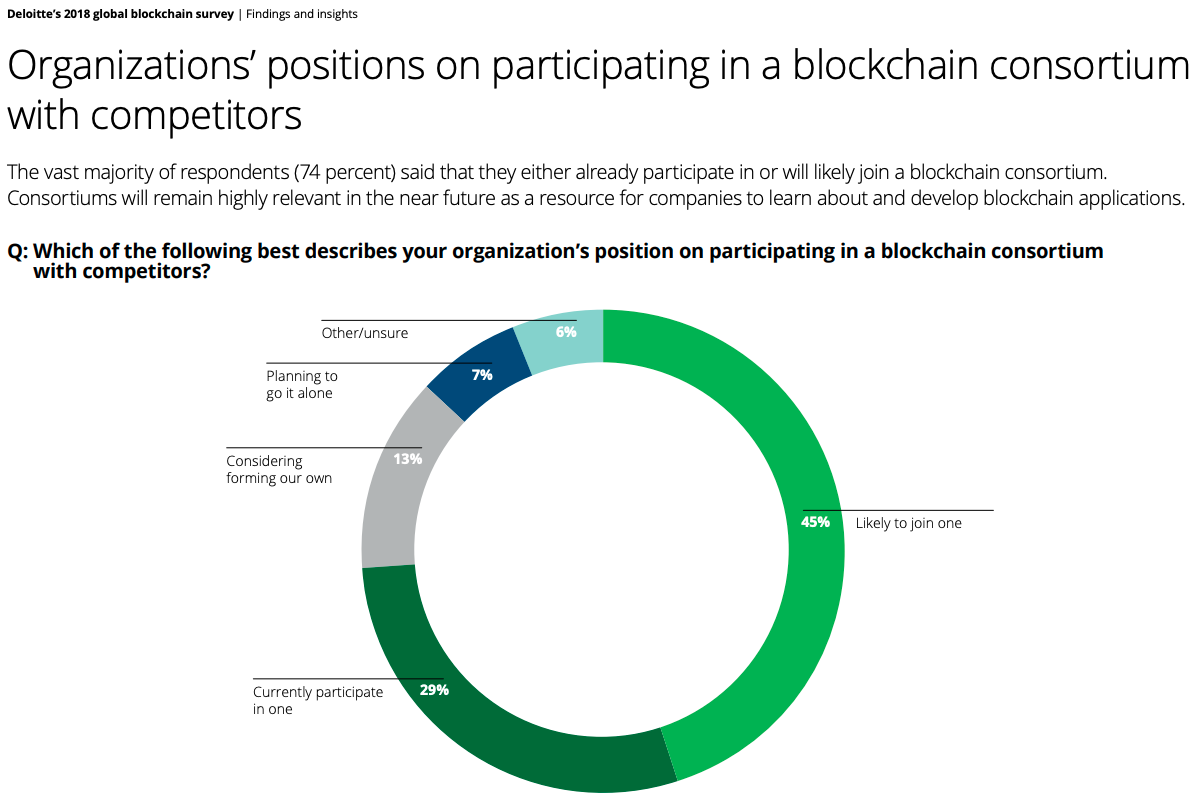

According to Deloitte’s 2018 Global Blockchain Survey, 29% of businesses polled stated that they’ve already joined a blockchain consortium, 45% stated they are likely to join one within the next year and 13% say they’re interested in starting a consortium of their own. In many cases, consortium members are fierce competitors. For example, Bank of America, Citi, Barclays, Morgan Stanley and other multinational banking institutions are members of the R3 consortium.

So what’s the motivation for these competing business to work together? The benefits of working together to better understand and improve blockchain technology are just too great. By working at the consortia level, these businesses share costs, create unified industry standards and expedite innovation by leveraging scale.

Thanks to the work done by enterprise organizations and blockchain startups at the consortium level, many concerns regarding blockchain technology have been greatly dissipated and as a result, the benefits of this revolutionary new technology will be felt much sooner.

In fact, blockchain technology is powering systems across the globe right now.

While blockchain technology might not be a part of your day-to-day life quite yet, it’s important to understand the technology and its developments. As we discussed above, many organizations have been working on a global scale to develop and deploy decentralized proofs of concept focused on improving transparency, accelerating the speed at which business is conducted, reducing fraud, and increasing the efficiency of public infrastructure such as electrical grids.

Blockchain and distributed ledger technologies can be confusing but the first step in understanding its potential impact is comprehending the advantages of this system at the most basic level. One of our partners, GoChain, recently published A Cryptocurrency Transaction is Very Similar to a Paper Check, a piece that does a great job breaking down the processes surrounding a crypto transaction in its most simple form while highlighting the differences and advantages provided by blockchain technology. Applicature has done the same thing regarding the supply chain with their blog, How to Apply Blockchain to Supply-Chain Management. Once you understand blockchain technology including its benefits and limitations, you can follow a systematic approach to evaluate whether blockchain is suitable for your business; Deloitte’s seven-step ideation process for developing blockchain use cases is one place to start.

It’s telling that nearly every day, enterprises and government agencies are announcing blockchain initiatives and proofs of concept. Target, Walmart, AT&T, Starbucks are a few examples, with the latest buzz being about Libra, Facebook’s cryptocurrency that is slated to launch next year with a list of founding members that includes Mastercard, Visa, Stripe, PayPal, Uber, Lyft, Spotify and eBay.

A few weeks ago we took a look at more than 20 banking and financial institutions to understand how they’re using and exploring blockchain technology, who they’re working with and what processes they’re working to improve. In many cases, what started as an internal proof of concept between business partners is now being used as part of day-to-day operations and saving organizations millions of dollars in operating expenses.

Business adoption isn’t limited to banking and finance. The Food and Drug Administration recently announced that they’ve partnered with IBM, Walmart, KPMG and Merck to implement a blockchain network to share and track data on the distribution of prescription drugs. This initiative aims to create real-time inventory tracking, increase the accuracy of data shared and reduce the volume of counterfeit drugs in circulation.

Blockchain technology is currently being leveraged within the energy sector as well regarding the coordination of distributed energy resources, green credit trading, wholesale energy trading, renewables development financing, and automated financial settlement. Blockchain technology is even disrupting the art industry. Did you ever think you’d be able to own part of an Andy Warhol painting?

While business adoption is being driven at the enterprise level (understandable given these large companies often have large budgets for R&D), businesses of all sizes are exploring the technology for B2B and B2C use cases. Small and medium-sized businesses may be in a better position to incorporate blockchain technology, with less bureaucracy and more willingness to run experiments, though tighter resources may be a limiting factor.

We recently began accepting applications for our private beta and are excited by the range in applicants, which include software developers, consultants, HR professionals, musicians, CEOs, product managers and students. They work in industries ranging from IT, transportation to finance, construction to food and beverage and in companies of various sizes — and are all interested in exploring blockchain technology to improve their businesses.

Myth: You need a computer science or cryptography degree to work with blockchain tech

“Blockchain Developer” was listed by LinkedIn as the number one emerging occupation in the U.S. last year, and we are seeing near-daily announcements of companies making their first blockchain hires (Square, Target) and sparing their blockchain teams during layoffs (IBM) we continue to see companies having difficulty filling new positions.

This is not surprising given the newness of the technology and the fact that most developers already have full-time jobs in addition to having to stay on top of all kinds of non-blockchain-related technology, which can make it difficult to develop the skills and experience to “hit the ground running” in a blockchain developer role.

“When companies are looking for developers, they are looking for professionals who have been involved in completed proof of concept (POC) projects, with skills required in Ethereum, Hyperledger Fabric and Corda Blockchain platforms,” said David Gadd, a Blockchain Talent Acquisition Consultant, when we asked him what companies are looking for when growing their blockchain teams.

The good news is that there are new tools being created and a continually growing list of educational/training programs to help those who want to take advantage of new opportunities. And while you don’t need a graduate degree in cryptography, you’ll at least need an understanding of cryptography, math, information security, the pros, cons and limitations of consensus models.

Are you a developer interested in experimenting with building applications that talk to blockchains? Please consider joining our private beta; it's free!

“There are many blockchain training opportunities, whether you decide to learn and study online or attend classroom training,” says Gadd. “Whenever there are new and emerging technologies, the training options are endless, but as always, ensure that the training has some credibility behind it.”

In addition to the growing number of courses, there are no shortage of tutorials by blockchain enthusiasts who wish to help fellow developers while helping make this technology become the norm. Side projects are a substantive way to demonstrate initiative and experience to prospective employers; if you’re a developer interested in creating a side project, we welcome you to sign up for our private developer beta to create applications that talk to blockchains.

At Esprezzo, it’s our mission to help developers and organizations that want to gain the benefits of blockchain technology for their businesses and products without needing to become experts in Solidity and without needing years of cryptography, blockchain and DevOps experience. If you’ve been looking for an opportunity to learn while creating blockchain-based applications, please consider joining our private beta.

October 2020 update: We recently announced Dispatch, a new no-code blockchain automation tool. Learn more about Dispatch.